Finding the best refinance mortgage rates in today’s market can mean the difference between saving thousands of dollars — or leaving money on the table.

Here’s a quick snapshot of current average refinance rates (as of May 2026):

Loan TypeAverage RateAverage APR30-year fixed refinance6.65%6.73%15-year fixed refinance6.03%6.10%30-year FHA refinance6.64%6.68%30-year VA refinance~6.03%-5-year ARM~6.42%-

Key takeaway: Rates have ranged from 5.98% to 6.89% over the past 12 months. That’s nearly a full percentage point of difference — which translates to hundreds of dollars per month on a typical loan.

For most homeowners, refinancing makes sense when you can lower your rate by at least 0.5% to 0.75% and you plan to stay in your home long enough to recover the closing costs (typically 2%–5% of the loan amount).

But rates alone don’t tell the whole story. Your credit score, your loan-to-value ratio, and the type of refinance you choose all shape the rate a lender will actually offer you — which can look very different from the national average you see advertised.

The Mortgage Bankers Association recently reported its Refinance Index was up 52% compared to a year ago. Homeowners are paying attention. The question is whether now is the right moment for you specifically — and how to make sure you’re not overpaying.

This guide breaks it all down.

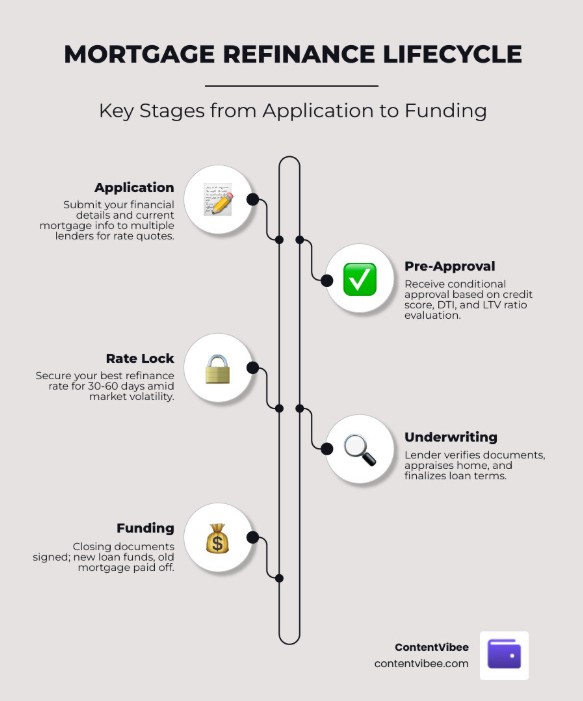

Strategies to Secure the Best Refinance Mortgage Rates

Securing the best refinance mortgage rates isn’t just about watching the news; it’s about presenting yourself as a low-risk borrower to the banks. Lenders use “risk-based pricing,” which means the rate you see on a billboard is usually reserved for someone with a near-perfect financial profile.

To understand what “best” truly means, we have to look at it through a lens of value. According to the Merriam-Webster definition of best, it implies the “greatest degree of good.” In the mortgage world, that means the lowest possible interest rate combined with the lowest fees.

The table below shows how much the loan term impacts your potential rate based on May 2026 averages:

Refinance TermAverage Interest Rate30-Year Fixed6.65%15-Year Fixed6.03%10-Year Fixed5.34%

As you can see, shorter terms generally offer a significant discount on interest, though they come with higher monthly payments.

Optimizing Your Financial Profile for the Best Refinance Mortgage Rates

If you want the “as low as” rates advertised by major lenders, your FICO score is the primary lever. Most lenders look for a score of 740 to 780 to unlock their top-tier pricing. If your score is currently in the 600s, taking three to six months to pay down credit card balances and dispute errors on your credit report can save you tens of thousands of dollars over the life of the loan.

Managing your Debt-to-Income (DTI) ratio is equally vital. Most conventional loans prefer a DTI below 36% to 43%. If you’re planning to refinance, avoid opening new credit cards or taking out auto loans, as these can negatively impact the pre-approval home loan process.

We also recommend weighing the cost of discount points. One point typically costs 1% of your loan amount and lowers your rate by about 0.25%. If you plan to stay in your home for ten years, paying for points is often a smart move. If you might move in three years, you’re better off taking a slightly higher rate to avoid the upfront cost.

Timing the Market and Economic Indicators

Mortgage rates don’t move in a vacuum. They are heavily influenced by the 10-year Treasury yield and Federal Reserve actions. While the Fed doesn’t set mortgage rates directly, its benchmark rate shifts the cost of borrowing across the entire economy.

Current trends show that market volatility is high. In early 2026, geopolitical tensions and fluctuating energy prices (with oil occasionally spiking over $100 a barrel) have kept rates in a state of flux. Even a small shift of 10 “basis points” (which is just 0.10%) can change your monthly payment. You can track historical mortgage rate trends and data through the Federal Reserve Bank of St. Louis (FRED) to see how today’s 6% range compares to the “outlier” 3% rates of the pandemic era.

Understanding Different Refinance Loan Types

Not every refinance is a simple “rate-and-term” swap. Depending on your goals, you might choose:

- Cash-Out Refinance: Replacing your loan with a larger one and taking the difference in cash. This is popular for home improvements, though it often carries a slightly higher interest rate.

- VA IRRRL: For veterans, the Interest Rate Reduction Refinance Loan is a “streamline” option that requires very little paperwork and no new appraisal.

- FHA Streamline: Similar to the VA version, this helps FHA borrowers drop their rates quickly.

- Military Choice: Some credit unions offer specialized products for those who haven’t built up 20% equity yet.

Navigating these choices is a key part of understanding the real estate buying process and long-term ownership strategy.

Evaluating the Costs and Long-Term Savings

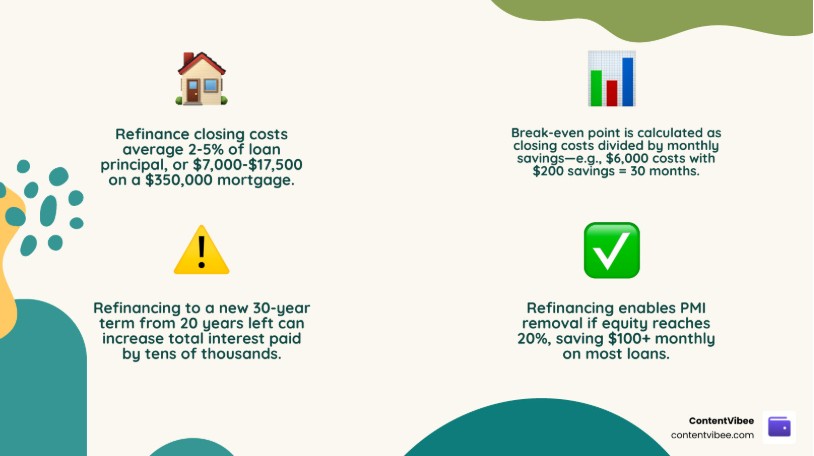

It’s easy to get blinded by a lower interest rate, but you must account for the “entry fee” of refinancing: closing costs. On average, you can expect to pay between 2% and 5% of your loan principal. On a $350,000 mortgage, that’s $7,000 to $17,500.

Before you sign, ensure you are dealing with a legitimate lender. Digital banking has made the process faster, but it has also opened doors for criminals. We always advise homeowners to read up on how to identify mortgage and wire transfer fraud to ensure their equity stays safe. You should also familiarize yourself with the average refi closing costs so you can spot “junk fees” on your Loan Estimate.

Calculating Your Break-Even Point

The “break-even point” is the moment your monthly savings finally surpass the amount you spent on closing costs.

Example:

- Closing costs: $6,000

- Monthly savings: $200

- Break-even: 30 months (2.5 years)

If you plan to sell the house in two years, this refinance would actually lose you $1,200. However, if you’re staying for a decade, you’ll net $18,000 in savings after the break-even point. Costs vary by region, so it’s worth looking at what the average closing costs are in Virginia or your specific state to get an accurate estimate.

Risks and Rewards of the Best Refinance Mortgage Rates

One common pitfall is extending your loan term. If you have 20 years left on a 30-year mortgage and you refinance into a new 30-year term, you might lower your monthly payment but end up paying significantly more in total interest over those extra ten years.

On the reward side, a refinance is an excellent time to eliminate Private Mortgage Insurance (PMI). If your home has appreciated in value and you now own 20% or more of the equity, refinancing into a conventional loan can delete that monthly PMI fee, even if the interest rate stays the same!

Throughout this digital journey, keep your guard up. Protecting your data is just as important as protecting your equity. We recommend visiting our finance category for tips on protecting your identity during the digital loan application process. From verifying lender credentials to using secure portals, staying safe in the digital age is a non-negotiable part of smart money management.

Conclusion: Taking Action with ContentVibee

Hunting down the best refinance mortgage rates requires a mix of market timing, personal financial discipline, and a healthy dose of skepticism. Don’t settle for the first offer you receive. Research shows that comparing quotes from just three to five lenders can save you an average of $80,000 over the life of a 30-year loan.

At ContentVibee, we believe in empowering American homeowners with practical, tech-forward advice. Whether you are calculating your break-even point or looking for more info about finance services and fraud protection, we are here to help you navigate the complexities of the 2026 housing market.

Ready to see if the math works for you? Start by gathering your current mortgage statement, checking your credit score for free, and using a secure calculator to see how much a 0.5% drop could change your life. Your future self — and your bank account — will thank you.