Rental house refinance rates are running 1–2% higher than primary residence rates right now — and knowing exactly what that means for your wallet is the first step to making a smart move.

Here’s a quick snapshot of what investors are seeing in May 2026:

Loan TypePrimary Residence Rate (Est.)Rental Property Rate (Est.)30-year fixed~6.47%~7.25–8.00%15-year fixed~5.75%~6.50–7.25%30-year conventional (Navy Federal)~5.625%Higher (varies)VA 30-year (Navy Federal)~5.250%N/A (primary only)DSCR loan (non-QM)N/A~7.50–8.25%

Key facts at a glance:

- Rental property refinance rates are typically 0.5% to 2% above primary home rates

- Most lenders require a credit score of 740+ for the best pricing

- You’ll need at least 25% equity (75% LTV or lower) to qualify for competitive rates

- Closing costs run 2–5% of the new loan amount

- A standard seasoning period of 6–12 months is required before most cash-out refinances

So why does this matter so much right now? Because millions of rental property owners are sitting on significant equity — U.S. median home prices reached roughly $425,000 in 2026 — while carrying loans originated at very different rate environments. Refinancing could either save you thousands or cost you more than you gain, depending entirely on your timing, loan type, and financial profile.

This guide breaks down everything you need to make that call with confidence.

Understanding current rental house refinance rates and eligibility

As we navigate the 2026 real estate market, we’ve noticed a significant shift in how lenders view non-owner-occupied properties. Unlike your primary residence, where a lender feels confident you’ll do anything to keep the roof over your head, rental properties are viewed as higher risk. If a tenant stops paying rent, a landlord is statistically more likely to default on that mortgage before their own home.

Risk-Based Pricing and the “Investor Spread”

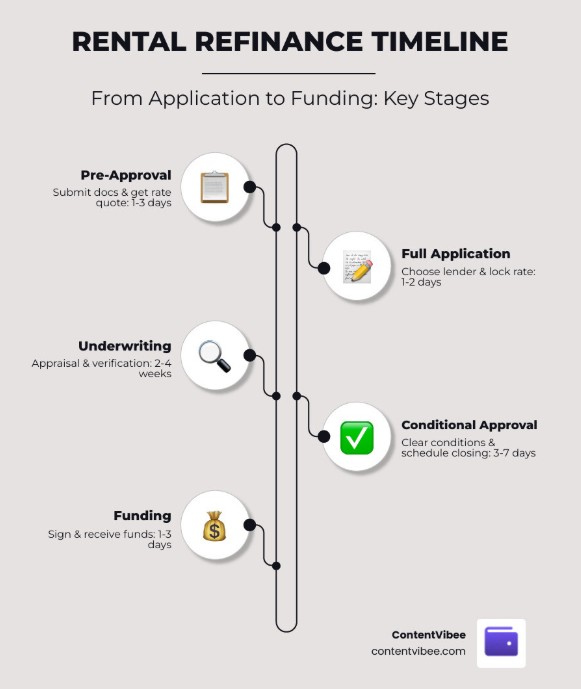

Lenders use what we call “risk-based pricing.” This means the rental house refinance rates you are offered aren’t just based on the daily market; they are adjusted based on the specific risks of your deal. Typically, you can expect a 1% to 2% rate premium over primary residence rates. For example, if your neighbor refinances their home at 6.5%, you might be looking at 7.5% or 8% for your rental property down the street.

Loan-to-Value (LTV) Ratios

Equity is your best friend in 2026. While you might be able to refinance a primary home with very little equity, rental properties usually require a “cushion.” For a standard rate-and-term refinance, most lenders cap the LTV at 75% to 80%. If you want a cash-out refinance, that cap often drops to 70% or 75%.

Key factors influencing rental house refinance rates

To snag the best possible terms, you need to look like the “perfect” borrower on paper. In our experience at ContentVibee, the difference between a 680 and a 740 credit score can mean thousands of dollars in interest over the life of the loan.

- Credit Score: Aim for 740+. While you can qualify with a 620-680, you’ll pay for it in the form of higher rates or extra “points” (prepaid interest).

- Debt-to-Income (DTI): For conventional loans, lenders look at your total monthly debt compared to your gross income. Most prefer a DTI of 36% or lower, though some stretch to 45% if you have high cash reserves.

- Debt Service Coverage Ratio (DSCR): This is a game-changer for 2026. Instead of looking at your personal income, lenders look at the property’s income. If the rent covers the mortgage, taxes, and insurance (usually a ratio of 1.2 or higher), you can qualify without showing W-2s.

- Property Type: Single-family homes generally get the lowest rates. Condos and multi-unit properties (2-4 units) are considered higher risk and often come with a 0.125% to 0.5% rate bump.

Understanding these requirements is part of the Pre Approval Home Loan Process which helps you set realistic expectations. If you are new to this, Understanding The Real Estate Buying Process can provide more context on how these numbers interact.

Comparing loan types for investment properties

Not all refinances are created equal. Depending on your goals — whether it’s lowering a monthly payment or pulling cash for the next deal — you have several paths:

- Conventional Fixed-Rate: The gold standard. These offer stability with 15- or 30-year terms. They follow Fannie Mae and Freddie Mac guidelines and usually offer the lowest rental house refinance rates.

- DSCR Loans: Perfect for the “scaling” investor. These skip the personal income verification, making them ideal if you own multiple properties and your tax returns are complex.

- VA IRRRL: If you are a veteran and originally bought a home with a VA loan that you now rent out, you may be eligible for an Interest Rate Reduction Refinance Loan (IRRRL). It’s one of the few ways to get “primary-style” rates on a rental.

- HELOCs: A Home Equity Line of Credit can be a powerful alternative. Some investors choose to keep their low-rate first mortgage and simply add a HELOC to tap into equity. We’ve found that Using a HELOC to Buy a Rental Property: Numbers That Actually Work is a strategy many of our readers are using to bridge the gap between properties.

If you’re still wondering Can You Really Buy Investment Property in this high-rate environment, the answer is yes — if you leverage the right loan product for your specific cash flow needs.

Managing closing costs and fees

Refinancing isn’t free. On average, you should budget between 2% and 5% of the loan amount for closing costs. On a $300,000 loan, that’s $6,000 to $15,000.

Common fees include:

- Origination Fees: Usually 1% of the loan amount.

- Discount Points: Optional fees you pay upfront to “buy down” your interest rate.

- Appraisal: Expect to pay $500-$800 for a professional to verify your rental’s value.

- Title Insurance and Escrow: These protect the lender’s interest in the property.

You can find more detailed breakdowns in our guides on Average Refi Closing Costs and What Are The Average Closing Costs In Virginia. To minimize these, we recommend shopping at least three different lenders — specifically comparing the APR (Annual Percentage Rate) rather than just the base interest rate.

Strategic timing and financial impact of a refinance

When does it actually make sense to pull the trigger? We suggest a “break-even analysis.” If your new loan saves you $200 a month, but costs $6,000 in fees, it will take you 30 months to break even. If you plan to sell the property in two years, that refinance is a losing move.

However, in 2026, many investors are refinancing not just for the rate, but for cash flow optimization. Lowering your monthly obligation even slightly can provide the “breathing room” needed to handle maintenance or vacancies. If you are considering a transition, check out our guide on Rental Property Sale What You Need To Know.

Cash-out vs. rate-and-term rental house refinance rates

A rate-and-term refinance simply changes your interest rate or the length of your loan. A cash-out refinance, however, allows you to tap into your equity to receive a lump sum of cash.

- The BRRRR Method: (Buy, Rehab, Rent, Refinance, Repeat). Investors use cash-out refinances to pull their initial capital back out of a property after improving it.

- Debt Consolidation: If you have high-interest business debt (10-20% APR), rolling that into a 7.5% mortgage can drastically improve your overall financial health.

- Improvements: Using equity to fund a kitchen remodel can allow you to raise the rent, often increasing the property’s value more than the cost of the loan.

Before you tap into that equity, be sure to understand the tax side of things. We cover this in Rental Sale Capital Gains Explained and Why Selling Investment Property Capital Gains Tax.

Navigating the 2026 lending landscape

The digital age has made refinancing faster, but it has also opened the door to new risks. In 2026, we see more sophisticated phishing attempts targeting mortgage applicants.

When shopping for rental house refinance rates, always use secure portals to upload your sensitive documents like tax returns and bank statements. Protecting your financial identity is just as important as finding a low rate. At ContentVibee, we prioritize your security by providing vetted Smart Money & Tech Tips for Americans.

One final expert tip: Interest Tracing. If you do a cash-out refinance, the IRS requires you to “trace” where that money goes. If you use the cash to buy another rental, that interest is generally deductible on your Schedule E. If you use it to buy a boat, it isn’t. Keep your funds in a separate account until they are deployed to ensure your tax professional can maximize your deductions.

Summary Checklist for Your Rental Refinance

- [ ] Check your credit score (Aim for 740+).

- [ ] Calculate your current LTV (Aim for <75%).

- [ ] Gather two years of tax returns and current leases.

- [ ] Compare at least three lenders (Bank, Credit Union, Mortgage Broker).

- [ ] Run a break-even analysis on the closing costs.

Refinancing a rental property is a business decision, not an emotional one. By focusing on the numbers and staying vigilant about your financial security, you can turn your property’s equity into a powerful engine for wealth building in 2026. For more help navigating these complex decisions, explore our latest finance and security resources.